Friday, January 31, 2014

Personal Finance Review

You’ll need to earn $2.00 for every $1.00 you want to spend assuming you pay 50% of your earnings on income tax, social security and Medicare. On the other hand, you get to keep 100% of every dollar you save on your personal expenses because the taxes have already been paid.

Periodically, review your expenditures with the diligence of an exuberant IRS agent on commission. It’s an exercise that most people don’t feel they have time to do but the rewards make it entirely worthwhile.

- Get comparative quotes on insurance – car, home, other

- Review and compare utility providers

- Review plans on cell phones

- Review plans on cable TV, satellite for unused channels and packages or receivers

- Review available discounts on property taxes

- Consider refinancing home – lower rate, shorter term or cash out to payoff higher rate loans

- Consider refinancing cars

- Call credit card companies to ask for a lower rate

- Review all of the automatic charges on your credit cards – consider no-fee cards

- Search for late fees that are regularly being paid and eliminate them.

- Review all bank charges for accounts and debit cards; determine if they can be reduced or eliminated.

If you don’t want to review your credit card accounts, consider reporting the cards stolen so that new numbers will be issued. You can notify the companies that need your number. Companies who might have your number won’t be able to automatically renew services that you may no longer be using. You can be assured that they’ll contact you when the old number doesn’t go through and you can re-evaluate the decision at that time.

Friday, January 24, 2014

Interviewing a Mover

“I’d wish I’d know that before I made a decision.” If you’ve ever regrettably said this to yourself, having a checklist might have prevented the issue in the first place. This list of questions can provide you with things to discuss when interviewing a moving company.

Fees

- What is the charge for packing?

- Does it include boxes? If not, what do they cost and will you deliver them?

- Is there an additional charge to deliver some items to a storage unit?

Insurance

- How is a damage claim handled?

- What insurance do you provide and is there a cost?

- Does the insurance cover items packed by the owner?

- Can additional insurance be purchased?

- If items are covered by my Homeowner’s insurance, whose insurance pays first?

Unusual Items

- Can you ship my car(s)? Will they be in the moving van or towed?

- What are the charges for shipping cars, lawn tractors, etc?

- What items cannot be shipped?

- If a shuttle truck is needed because of the location of my house or size of the drive way, is there an additional charge?

- If packing and loading are on different days, can you leave the beds and other basics out for us to use?

Dates

- What dates are available for our move?

- What date will you pack and how long will this take?

- What date will you load the van?

- What date will the van arrive at my new location?

- If my new home is not ready for delivery, how many days can it be delayed before there is a charge?

- What is the charge for additional days or weeks?

Terms

- Are there any additional fees that I’m responsible for that have not been discussed?

- What are the terms of payment?

- Is a down payment required?

- When will the balance be due and who is authorized to accept it?

Friday, January 17, 2014

What Can You Expect?

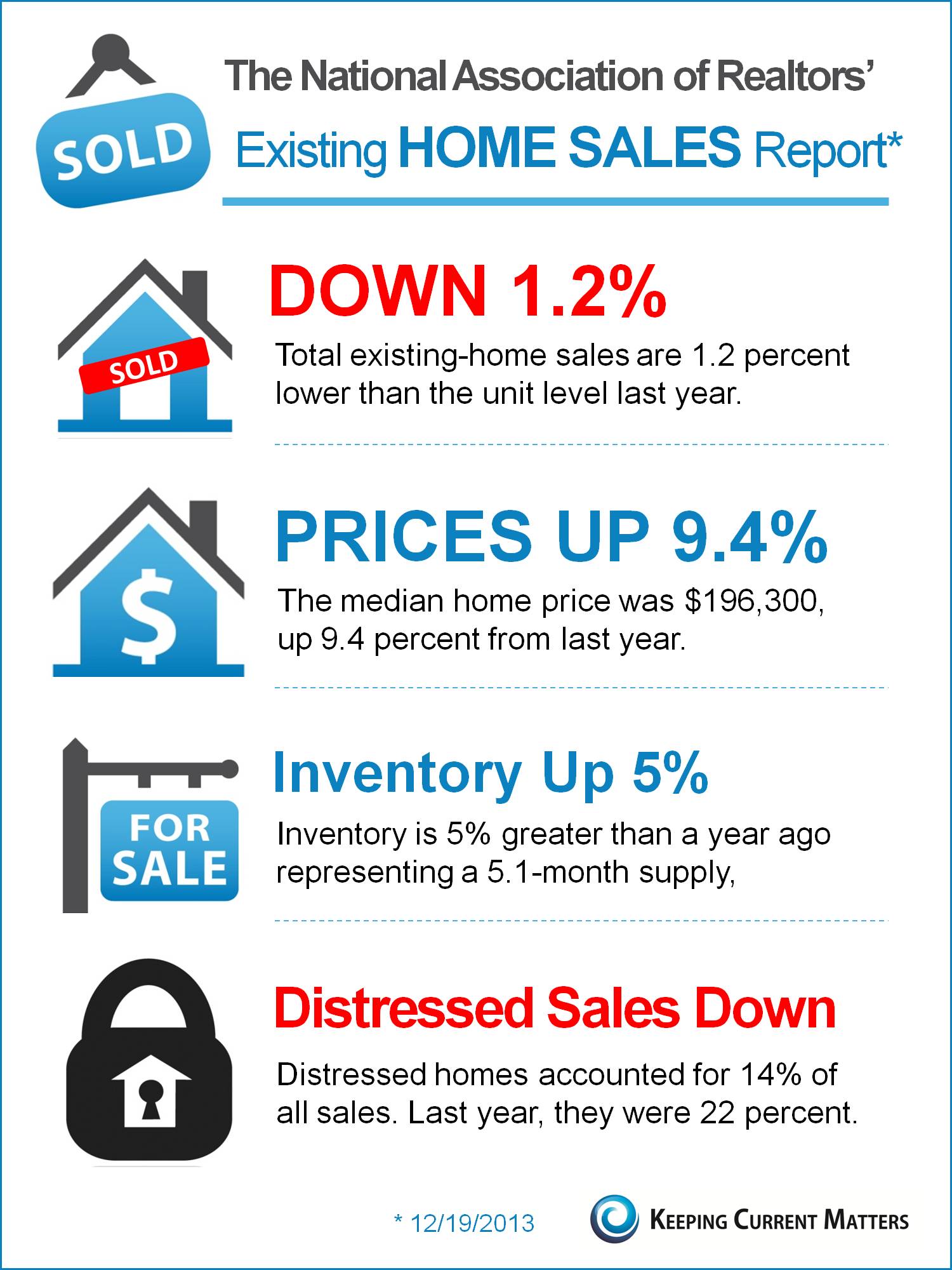

The two most frequently quoted constants in life are death and taxes. Two more things would-be homeowners can expect in the near future are increases in mortgage rates and housing prices.

Interest rates have been kept artificially low for several years by the Federal Reserve in an effort to strengthen the economy. Policy is shifting to allow them to seek their own natural level and that will surely result in higher mortgage rates. Rates on 30 year fixed mortgages are up over 1% from January, 2013.

Foreclosure activity is down, new home starts are up and prices have been increasing in most markets for two years. Most experts agree that the cost of housing is going up.

{kind=link}

If the price were to go up by 2% and the mortgage rate by 1% while a buyer is “sitting on the fence” making a decision, the payment would go up by almost $175.00 each and every month for the term of the mortgage. Even if a person can afford to make the higher payments, what could they have done with that extra $175.00 a month? Buy furniture? Car payment? Principal reduction? Retirement contribution? Save for a rainy day?

Click here to determine what the cost of waiting to buy will be using your price home.

Tuesday, January 14, 2014

Monday, January 13, 2014

Friday, January 10, 2014

What Kind of Showing Was It?

One of the most frequent calls from homeowners to their agents is about the listing’s inactivity due to the lack of showings. The homeowner commonly believes that the home is shown only when a buyer walks through the house with an agent.

Today’s buyers are more sophisticated than in the past due to the abundance of information available to the public on the Internet. There are seemingly inexhaustible sites with homes for sale, valuation estimates and virtual tours. There are extensive mapping sites with satellite images, traffic conditions, entertainment, shopping and other points of interest.

There are actually three legitimate types of property showings. A knowledgeable buyer can view a home for sale online and make a reasonable determination of whether the home will fit their needs. Occasionally, buyers will drive by a home to get a feel for the home and also the neighborhood which might cause them to eliminate any further examination or consideration.

The third type, the physical showing, certainly gives the buyer the opportunity for the closest scrutiny but is generally reserved for properties that have passed the inspections of at least one other type of showing.

Sellers should be aware of the different types of showings and that a sales agent’s job is to help the buyer find the right home. The listing agent’s job is to market the home so that the right buyer finds it either through their own efforts or that of the buyer’s agent.

Tuesday, January 7, 2014

Friday, January 3, 2014

Can You See the Savings?

If you’ve considered changing your light bulbs to energy-saving LED bulbs but decided not to make the investment because the prices were too high, you might want to investigate again. The prices have come down considerably.

An initial investment now will generate immediate returns through energy costs and because they last longer, you won’t need to replace them for years.

The life of LED bulbs is projected to be from 35,000 to 50,000 hours compared to an incandescent bulb at 750 to 2,000 hours. For normal home use, a LED bulb could last more than 20 years.

80-90% of the energy used by fluorescent and incandescent bulbs is wasted by the heat generated. In contrast, cool LED bulbs converts 80% of the electrical energy to light energy.

• The color of LED lights is bright white, more like daylight, instead of the warm yellow of incandescent or the greenish tint of fluorescent bulbs.

• LEDs light up instantly instead of building to their intensity like some of the fluorescent bulbs.

• LEDs are more durable because they don’t have filaments or thin-glass bulbs like incandescent and fluorescent bulbs.

Shop around to find the best price on LEDs. If the LED only lasted 20,000 hours, you might have to purchase 20 incandescent bulbs during that same period of time. Using the chart below, you can see that the LED uses about 10% of the wattage without compromising on the brightness.

Subscribe to:

Posts (Atom)